ANNUAL COMPLIANCE OBLIGATION 2023

As the financial year 2022 has ended on 31st December 2022 and now enterprises registered in Cambodia are supposed to finish their annual compliance obligations. We would like to summarize the annual compliance obligations with the recent changes as below:

Lochan & Co

Chartered Accountants

LABOUR COMPLIANCE

FOREIGN EMPLOYEE QUOTA FOR 2023

Enterprises employing or intending to employ foreign employees are required to apply for a foreign employee quota via the Ministry of Labour and Vocational Training (“MLVT”) online system. All applications must be submitted by the required deadline each year. Typically, the foreign employee quota application window is open from early September to 30 November each year for the use of foreign employees in the following year.The deadline for the 2023 application is extended to the end of January 2023. According to Joint Prakas659, if an enterprise hires foreignemployee(s) without the approved quota,it may be subject to a fine of up to KHR 2.52 million (approximately USO630) by the MLVT or KHR3.6 million (approximately USO 900) by the court. Please note that fines may be imposed in triple in the event of repeated offenses. Additional sanctions, as imposed by the Labour Law, in clude terms of imprisonment from six days to one month.To our knowledge to date, terms of imprisonment have yet to be strictly enforced.

FOREIGN EMPLOYEE QUOTA FOR 2023

A foreign national must holda valid work permit in order to lawfully work in Cambodia. A work permit for foreign employees is valid for only one year. No matter when the work permit for foreign employees is issued by the MLVT/DLVT, it expires on 31 December of that year.If an enterprise continues to employ foreign nationals in Cambodia for the following year, the enterprise needs to apply for an extension of their foreign work permits by 31 March of the following year. While pursuant to Prakash 352, a work permit or an extension thereof can be requested online, foreign employees may also be called to present themselves in person before the MLVT after submission of their work permit applications subject to the discretion of the MLVT.

NATIONAL SOCIAL SECURITY FUND ("NSSF")

An enterprise employing one or more employees is required to register itself and all of its employees with the NSSF within30 days after the date of its opening. Once registered, the enterprise must pay a monthly contribution to (a) occupational risk insurance (work-related accidents and occupational diseases);and (b) health care insurance (c) pension scheme. The pension scheme has been implemented from July 2022, although the contribution payment has effectively commenced from October 2022. Each registered enterprise must pay the contribution by the 15th of each month and report to the NSSF on the number of employees before the 20th of each month. These dates may be changed subject to periodic notifications issued by the NSSF. The monthly contribution for the pension scheme must be made together with contributions for the occupational risk and health care schemes.

SENIORITY PAV FOR EMPLOYEESUNDER UNSPECIFIED DURATION CONTRACT ("UDC")

Seniority pay equal to 15 days of wages and other bonus per year must be paid to employees who are employed under UDCs during on-going employment every six months per year, divided into 7.5 days of wages and other benefits to be paid in June and 7.5 days of wages and other benefits to be paid in December.

LARCE EMPLOYER OBLICATIONS

When an enterprise employs 100 or more employees, the company must employ 1% of its total work force as qualified disabled persons and report to the MLVT and the Ministry of Social Affairs,Veteran and Youth Rehabilitation in January each year.

An enterprise employing more than 60 employees is required to conduct annual training of apprentices based on the following quota in proportion to the enterprise’s total workforce:

-10% for enterprise that employs between 61 to 200 employees.

– 8% for enterprise that employs between201 to 500 employees.

– an additional 4% for every further 500 employees at the enterprise that employs more than 51 employees, provided that a maximum of 110 apprentices may be trained by an enterprise in one year.

The deadline for fulfilling the training of apprentices is 31 October each year.

It is important to note that the enterprises that have not fulfilled the obligations regarding the training of apprentice must submit a request to the MLVT for payment of tax in lieu of training the apprentices, in an amount equivalent to 1% of total annual salary of all employees per year.

2022 TAX ON INCOME RETURN

The standard tax year in Cambodia runs from l January to 31 December 2022. Electronic filing for the 2022 annual Tax onIncome (TOI) declaration with the General Department of Taxation (GDT) must be completed by the 31st of March 2023, or within three months after the end of the tax year for enterprises that have a non-standard tax year.

Those self-assessment taxpayers (taxpayers that are registered with the GDT) that have local branches are required to file a consolidated 2022 TOI declaration attaching the financials of the respective local branches with the return.

Self-assessment taxpayers that have both Qualified Investment Project (QIP) and non-QIP activities are required to submit their annual 2022 TOI return by Prakas 1127 MEF.P dated 11 October 2016.

All self-assessment taxpayers filing annual 2022 TOI returns with the GOT are required to include a balance sheet, profit and loss account, and an annexed list of any related party transactions carried out during the 2022 tax year.

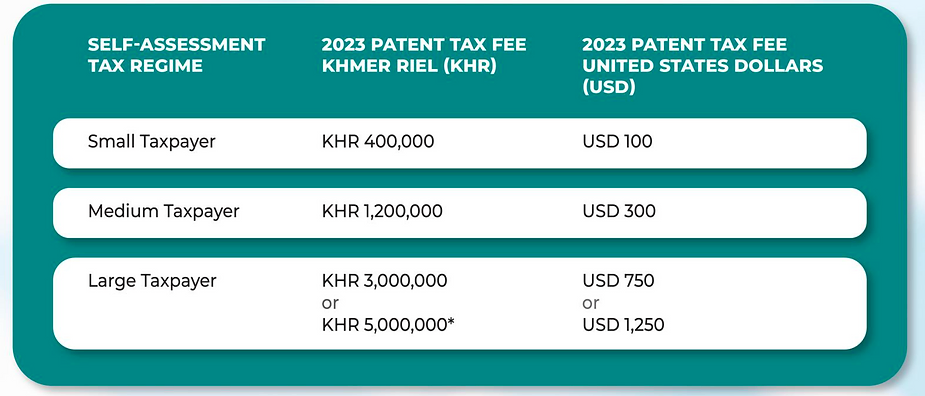

2023 PATENT TAX

All self-assessment taxpayers operating in Cambodia are required to register and pay their2023 Patent Tax by the 31st of March 2023 foreach business activity that they carry out. The amount of Patent Tax payable in 2023 is dependent on the particular classification of the enterprise under the Self-AssessmentRegime of Taxation. The 2023 Patent Tax fees are as follows:

*If the annual turnover of the LargeTaxpayer exceeds KHR 70,000 million (USO 2.5 million) then the Patent Tax payable will be USO 7,250. If the annual turnover of the LargeTaxpayer is less than KHR 70,000 million (USO 2.5 million) the Patent Tax payable will be USO 750.

SUBMISSION OF ANNUAL FINANCIAL STATEMENTS

AUDITED FINANCIAL STATEMENTS

Entities who are required to obtain audited financial statements under Prakas 563 (please refer to the criteria} are required to submit their audited financial statements with the Accounting and Auditing Regulator (ACAR), using its e-filing system, no later than 6 months and15 days after the close of the accounting period.

Those enterprises that fail to submit their annual financial statements in time to ACAR as per Instruction 002 will be subject to penalties as provided in Sub-Decree no. 79 dated 1 June 2020.

UNAUDITED FINANCIAL STATEMENTS

Under the newly implemented Instruction No.002 AAR.N those entities that arenot required to have their 2022 financial statements externally audited under Prakas 563, are now required to submit their 2022 unaudited financial statements through ACAR’s e-filing system no later than 3 months and15 days after the close of the accounting period which for most entities will be by15 April 2023.

Those enterprises that fail to submit theirannual financial statements in time to ACAR as per Instruction 002 will be subject to penalties as provided in Sub-Decree no. 79 datedl June 2020.

NOTIFICATION RECARDING USE OF ENGLISH

Notification 057AAR, dated21 July 2022, required enterprises that have been registered before 21 July 2022to submit an application to ACAR for the use of English language in their accounting system before 31 December 2022.

For enterprises established after 21 July 2022 they are required to submit an application within 180daysfrom the date of theirregistration with theGOT.

Failure to comply withthe above obligations will result in penalties being imposed.

APPLICATION FOR ANNUAL CERTIFICATE OF COMPLIANCE

All enterprises registered in Cambodia that are recognized as a Qualified Investment Projects (“QIP”) are required to submit an application for a Certificate of Compliance (“COC”) to the Council for the Development of Cambodia by the 31st of March of each year following the year in which they obtained their Final Registration Certificate. If a company holding a QIP fails to obtain a COC it may lose its investment incentives.

ANNUAL DECLARATION OF COMMERCIAL ENTERPRISE

Following the issuance by the Ministry of Commerce (“MOC”) of Prakas No. 107 (MOC), the filing of Annual Declarations of Commercial Enterprises (“ADCE”) dated 5 April 2017, an ADCE must be submitted by each enterprise to the MOC using its online system.

Use of the on line system for submission of an ADCE is now compulsory and must be performed within three months from the anniversary of the enterprise’s re-registration on the MOC’s online system.

A submission made after the three months period, will be subjected to a penalty of KHR 2,000,000(approx. USD 500) imposed by the MOC.

NATIONAL DOMAIN NAMES

From 1January 2023 onwards, when filing an ADCE, all company registered in Cambodia must provide Ministry of Commerce (MOC) with an email address having a level 2 national domain name. If locally registered company does not have email address with level 2 national domain name, then it must apply for such domain name with the Telecommunication Regulator of Cambodia as soon as possible in order to comply with the requirements set out under Sub-Decree 287 dated 31 December 2021.

We at Lochan & Co, stand ready to answer any questions that you may have on any issue regarding monthly & annual compliances applicable to corporates registered in Cambodia.

DISCLAIMER

This document/material is not intended to provide definitive answers to specific individual/corporate circumstances and as such is not intended to be used as a guide. Lochan & Co recommends seeking independent expert advice relating directly to any specific situation. Lochan & Co accepts no responsibility for anyone placing sole reliance on this material.